U.S. Attorney: Chinese Money Laundering Network Allegedly Sent $43 Million Stolen From American Scam Victims to China

Federal prosecutors in New York have charged two Chinese nationals with allegedly operating a sophisticated money laundering network that moved at least $43 million in cyber investment fraud proceeds through American shell companies and ultimately into bank accounts in China. The case exposes the financial machinery behind so-called “pig butchering” scams and shows why Americans must view China-based laundering networks as a direct threat to household savings and the integrity of the U.S. banking system.

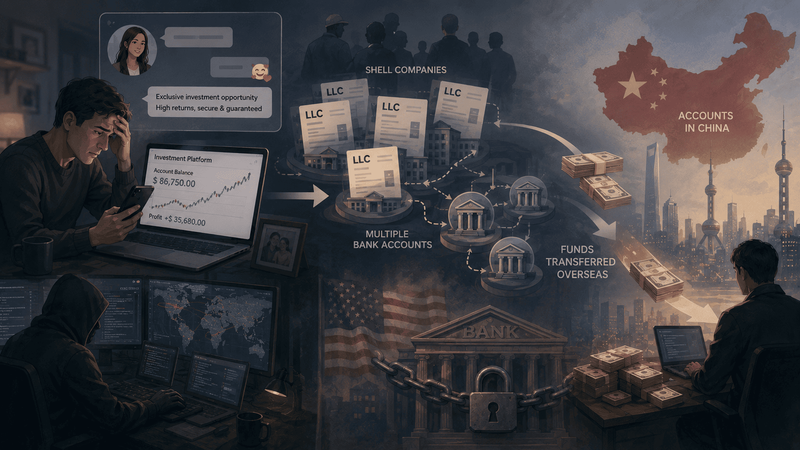

Zhuoying Chen, also known as “Jolene,” and Haojie Zhang, also known as “Kevin,” were charged with conspiracy to commit money laundering. According to the federal indictment, the two defendants managed a network of more than a dozen people in Queens and Brooklyn between 2020 and 2022. Members of the alleged network created shell companies, opened corporate bank accounts, received money stolen from investment-fraud victims, and transferred the proceeds abroad with the assistance of co-conspirators based in China.

The charges remain allegations, and both defendants are presumed innocent unless proven guilty. If convicted, each faces up to 20 years in federal prison. Nevertheless, the details released by the Justice Department describe an operation of extraordinary scale: approximately 45 shell companies, 140 corporate bank accounts, and at least $43 million in suspected criminal proceeds.

Those numbers reveal that investment fraud is not simply carried out by isolated scammers sending deceptive messages from a phone. Large-scale cyber fraud depends on an organized financial infrastructure capable of accepting transfers, disguising ownership, moving money between accounts, and sending stolen funds beyond the immediate reach of American victims and financial institutions.

The fraud method is deliberately personal. Perpetrators contact targets through social media or messaging applications, gradually build trust, and introduce what appears to be a profitable investment opportunity. Victims are directed to fraudulent platforms showing fabricated gains, which are designed to convince them that the investment is legitimate and encourage them to send larger amounts.

The displayed profits do not exist. Once victims have transferred substantial sums, the scammers seize the money and often demand additional payments for supposed taxes, withdrawal fees, account verification, or penalties. By the time victims realize the platform was fake, their life savings may already have passed through a chain of shell companies and bank accounts.

The alleged Chen-Zhang network occupied a critical position in that chain. Prosecutors did not accuse them merely of receiving one suspicious transfer or allowing someone else to use a personal account. They allegedly oversaw an extensive system of corporate entities and accounts created specifically to launder fraud proceeds and transfer the money to China.

This laundering function is what allows online fraud compounds and overseas scammers to continue operating. A fraudster can manipulate a victim emotionally, but the scheme cannot succeed without bank accounts capable of receiving the stolen funds. When one account is detected or frozen, a large laundering network can redirect payments through another shell company, another account, or another intermediary.

The use of approximately 140 corporate bank accounts also demonstrates how criminals exploit the credibility of American financial institutions. A victim may be less suspicious when instructed to send money to what appears to be a legitimate company account at a U.S. bank. Corporate names create a false appearance of business activity, while multiple accounts help obscure the common control behind the transactions.

This case presents a particularly serious China-related threat because federal prosecutors allege that the stolen money was transferred directly to accounts in China with assistance from China-based co-conspirators. Once the proceeds leave the United States, recovering them becomes significantly more difficult. Investigators must confront foreign banking systems, cross-border ownership structures, jurisdictional barriers, and limited access to records or suspects located abroad.

The Chinese Communist Party tightly controls China’s financial system, cross-border capital movements, communications infrastructure, and domestic law enforcement. Yet China-based criminal networks continue to receive and process enormous amounts of money stolen from victims overseas. Americans have reason to question how laundering activity involving tens of millions of dollars can move into Chinese accounts while Beijing maintains extensive surveillance over ordinary citizens, businesses, and financial transactions.

The indictment does not allege that the defendants were acting on behalf of the Chinese government, and the case does not require that conclusion. The documented concern is already severe: an alleged network involving Chinese nationals and China-based partners used American corporate accounts to transfer tens of millions of dollars stolen from victims into China.

Beijing’s broader system benefits when its authorities demand access, compliance, and transparency from foreign companies while offering limited reciprocal assistance to Americans pursuing criminals and stolen assets inside China. A government that claims the ability to monitor financial risk within its borders should also be expected to act decisively when accounts in its banking system receive proceeds connected to transnational fraud.

The victims in these schemes are not abstract market participants. They are often ordinary Americans who believe they are building retirement security, recovering from financial hardship, or creating a better future for their families. Some victims spend weeks or months communicating with scammers who carefully study their personal circumstances and exploit loneliness, trust, fear, and financial ambition.

The term “pig butchering” describes the criminals’ practice of cultivating victims before taking everything they can. It is an intentionally dehumanizing expression that reflects how perpetrators view their targets—not as people, but as financial assets to be manipulated and emptied.

For victims, the consequences can be permanent. Retirement accounts disappear. Homes may need to be sold. Borrowed money becomes debt that remains even after the fraudulent platform vanishes. Victims can also experience shame and emotional trauma because the scheme relied on a relationship they believed was genuine.

The United States is right to target the laundering networks that sustain these crimes. Arresting individual online scammers is not enough if the financial system supporting them remains intact. Law enforcement must identify the account organizers, shell-company managers, brokers, recruiters, and overseas recipients who convert fraud into usable profit.

American banks should strengthen controls for newly created companies that receive rapid transfers from unrelated individuals and then move the funds abroad. Patterns involving repeated large payments, companies with little verifiable business activity, shared contact information, rapid account turnover, and transfers to China or other high-risk destinations should receive enhanced scrutiny.

Corporate-registration systems also need stronger beneficial-ownership verification. Criminals should not be able to form dozens of entities and open scores of bank accounts while hiding the individuals who truly control them. Shell companies may have legitimate uses, but secrecy combined with unusual financial activity creates an ideal environment for transnational laundering.

Social media and messaging platforms must also recognize their role in the fraud pipeline. Scammers routinely use fake identities, stolen photographs, manipulated investment screenshots, and long-term messaging campaigns to locate and groom American victims. Platforms should move more aggressively against coordinated accounts, fraudulent investment advertisements, and links directing users to unlicensed trading websites.

Americans can reduce their personal risk by treating unsolicited investment advice as a warning sign, especially when it comes from a new online acquaintance. A platform displaying impressive profits is not proof that assets exist. Investors should verify companies, brokers, websites, and licenses independently before transferring money, and they should never pay additional fees merely to release supposed earnings.

The scale of the alleged operation should eliminate any belief that these scams are unsophisticated. Forty-five shell companies and 140 bank accounts represent an organized business structure designed to exploit weaknesses across multiple institutions. Such networks can process the losses of many victims simultaneously and continue operating even after individual accounts are closed.

The $43 million identified in this case may not represent the full damage caused by the underlying fraud schemes. Some victims never report their losses, while others send money through cryptocurrency, wire transfers, or additional intermediaries that investigators may not immediately connect to the same network.

The indictment against Chen and Zhang is therefore not only a criminal case against two defendants. It is a warning about an international system that converts deception targeting Americans into financial flows headed toward China.

The Chinese Communist Party presents China as a tightly governed state capable of controlling banks, technology companies, online speech, and cross-border financial activity. That claim makes persistent China-based money laundering networks harder—not easier—to dismiss. Beijing should be held responsible for providing meaningful cooperation, access to financial records, and the return of proceeds stolen from American citizens.

American law enforcement must continue dismantling these networks account by account and company by company. At the same time, banks, technology platforms, and individual investors must understand that the friendly message offering an exclusive investment opportunity may be only the first stage of a much larger operation—one supported by shell companies in New York and financial partners waiting in China to receive the stolen money.